2026 Retirement Plan Contribution Limits

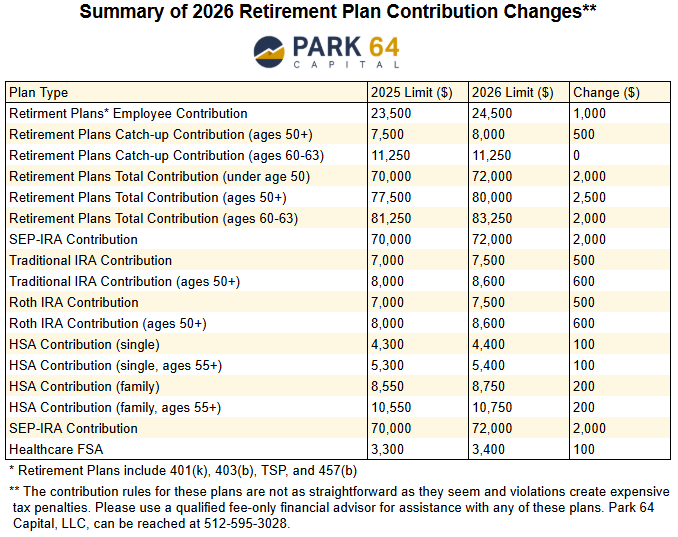

The IRS has made some notable changes to retirement plans in 2026, including an increase to the 401(k), 401(k) catch-up, IRA, and HSA contribution amounts. A summary table is below.

In many cases, application of these rules can be tricky, especially if you’re married, in a domestic partnership, have access to multiple plans, are self-employed, or lose plan access mid-year; the nuances of these cases are not covered here.

2026 401(k), 403(b), and TSP Employee Contribution Limit

The employee contribution limit for 401(k), 403(b), and TSP plans has increased from $23,500 in 2025 to $24,500 in 2026.

The catch-up contribution for those ages 50 and older has increased to $8,000 in 2026, which means employees ages 50 and older can contribute up to $32,500 in 2026.

The super catch-up contribution provision for those ages 60–63 remains at $11,250 in 2026, which means those ages 60–63 can contribute up to $35,750 in 2026.

2026 401(k), 403(b), and 401(a) Total Contribution Limit

The combined employee and employer contribution limit for 401(k), 403(b), and TSP plans has increased from $70,000 in 2025 to $72,000 in 2026.

For those ages 50 and older, including the catch-up contribution, the maximum is $80,000 in 2026.

For those ages 60–63, using the higher catch-up provision, the maximum is $83,250 in 2026.

2026 457(b) Total Contribution Limit

The employee contribution limit for 457(b) plans has increased from $23,500 in 2025 to $24,500 in 2026.

Remember, those with access to both a 401(k) and a 457(b) plan can max out both plans in the same year.

The 457(b) catch-up contribution for those ages 50 and older is $8,000 in 2026; check with your plan administrator to see if the “last-3-year catch-up” provision applies.

2026 Traditional IRA and Roth IRA Contribution Limit

The contribution limit for Traditional IRAs and Roth IRAs has increased from $7,000 in 2025 to $7,500 in 2026.

The catch-up provision for those ages 50 and older is now $1,100 in 2026.

2026 Traditional IRA Income Phaseout Limits

For those who are unmarried without a retirement plan at work, Traditional IRA contributions are fully deductible in 2025.

For those with a retirement plan at work, the tax deductibility of Traditional IRA contributions has the following income phaseout ranges:

Single (2025): $79,000-$89,000

Single (2026): $81,000–$91,000

Married Filing Jointly (2025): $126,000 - $146,000

Married Filing Jointly (2026): $129,000 - $149,000

If you are married but only your spouse is covered by a retirement plan, the following phaseout range applies to you:

2025: 236,000-$246,000

2026: 242,000-$252,000

2026 Roth IRA Income Phaseout Limits

The Roth IRA contribution eligibility ranges have also increased:

Single and Head of Household (2025): $150,000 - $165,000

Single and Head of Household (2026): $153,000–$168,000

Married Filing Jointly (2025): about $236,000–$246,000

Married Filing Jointly (2026): about $242,000–$252,000

2026 Health Savings Account (HSA) Contribution Limits

For 2026, the HSA contribution limits are:

Self-only coverage: $4,400, up from $4,300 in 2025

Family coverage: $8,750, up from $8,550 in 2025

The HSA catch-up contribution for those ages 55 and older remains $1,000. Remember that for families, each partner may put $1,000 of catch-up contribution into their own individual HSA, but not into the same HSA, for a total of $2,000.

2026 Flexible Spending Account (FSA) Contribution Limits

The healthcare FSA contribution limit for 2026 has increased to $3,400, up from $3,300 in 2025.

Dependent care FSAs have separate limits and are not the same as healthcare FSAs.

2026 SEP IRA Contribution Limits

The SEP IRA contribution limit has increased from $70,000 in 2025 to $72,000 in 2026. Remember, SEP IRA contributions can only be made by the employer.

SOURCE: https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500